Gold Price Surge in 2024: Geopolitical Tensions and Federal Reserve Rate Cut Speculations

Explore the factors driving the Gold Price Surge in 2024. Discover how geopolitical tensions and Federal Reserve rate cut speculations impact gold.

Zeynep Kucukkirali

4 Min Read

Oct 10, 2024

Undoubtedly, the shining star of 2024 has been gold. Gold prices have surged by approximately 30% this year, jumping to $2,685 per ounce before slightly retreating as expectations of interest rate cuts from the Federal Reserve reshaped. However, it continues to trade near historical highs.

The easing of high interest rate policies maintained by major global central banks following the pandemic, strong demand from central banks, global political uncertainties, and ongoing geopolitical risks have provided strong tailwinds for gold this year. Particularly in the final stretch, speculations regarding the extent of the Federal Reserve's interest rate cuts for this year have been the primary catalyst for movement in the gold market.

In August, surprising U.S. labor market data triggered fears of a recession. The unemployment rate jumped to its highest since October 2021, while job growth fell to its lowest since the pandemic. Heightened expectations for more aggressive rate cuts, driven by the belief that the Fed was late in starting rate cuts, propelled gold prices toward record levels.

However, recent data has quelled recession fears, and markets are now pricing in gradual Fed-rate cuts. While this has caused a significant loss of momentum in the gold market, strong safe-haven demand may continue to limit downward movements.

Geopolitical Tensions Boosting Gold Demand

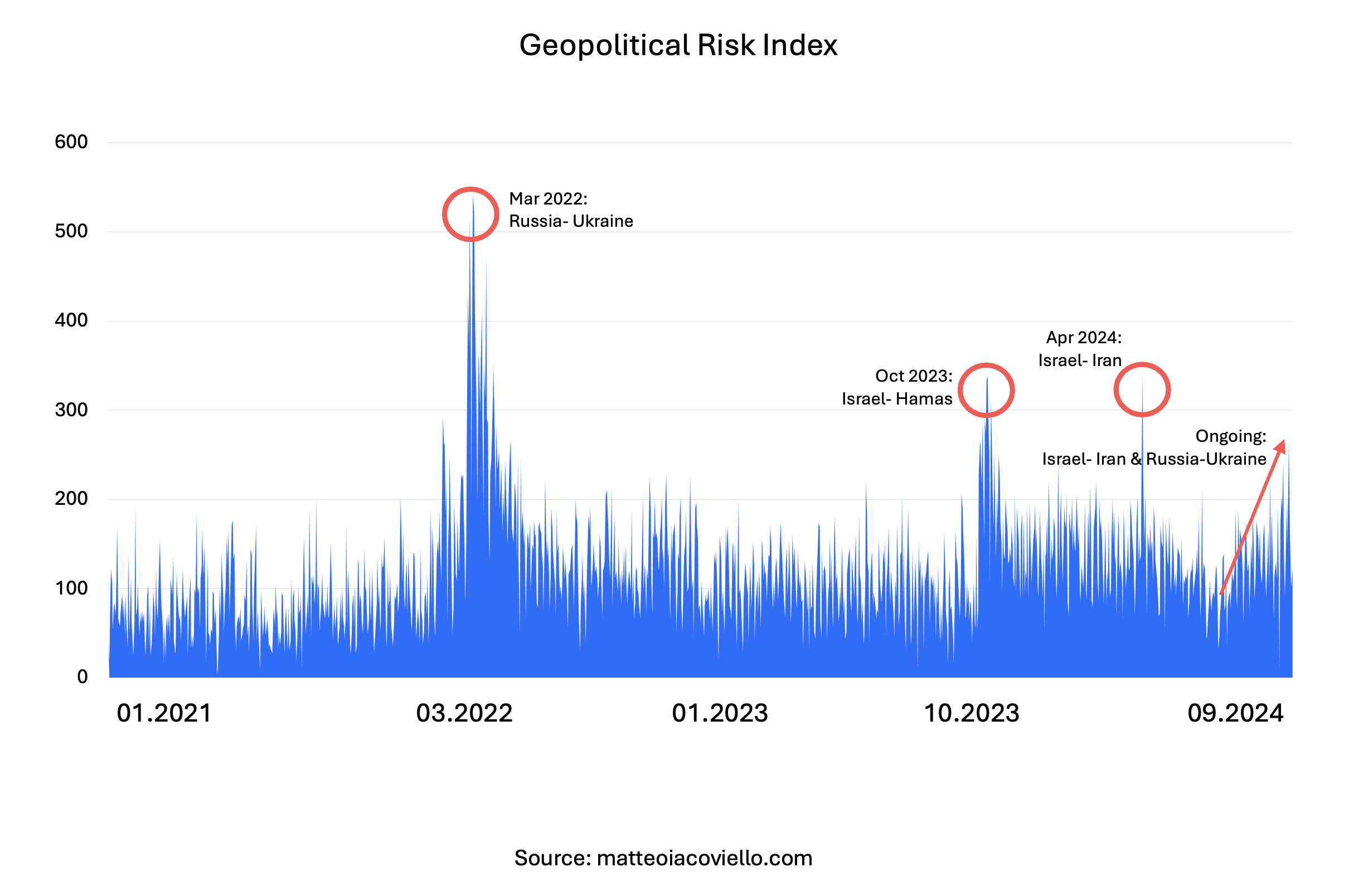

High geopolitical tensions have marked the year 2024. According to data from the Geopolitical Risk Index (GPR), the risk perception, which averaged 118 points in 2023, has increased by 12% to an average of 133 points in 2024 (as of October 7).

Tensions between Israel and Iran, which sharply escalated in April, continue with reciprocal attacks. Last week, following Iran’s missile strike on Israel, markets are now waiting for Israel’s response.

Meanwhile, the war between Ukraine and Russia, ongoing since 2022, persists in Eurasia. In early August, after Ukraine’s cross-border attack and Russia’s largest air strike since the war began, tensions remained elevated.

According to the World Gold Council’s (WGC) Gold Return Attribution Model (GRAM), geopolitical risks contributed 4.3% to gold’s return this year. Every 100-point increase in the GPR index is estimated to correspond to a 2.5% rise in gold prices.

In WGC's survey of global investors, geopolitical shifts and regional conflicts ranked as the third and fourth factors influencing investment decisions. When geopolitical risks remain elevated (typically when the GPR index is above 100), demand for gold as a safe haven remains strong.

In conclusion, unless ceasefires are seen in the Middle East and Eurasia conflicts, which are driving current geopolitical risks, they will likely continue to support demand for gold. Currently, geopolitical risks are limiting the pressure caused by expectations of slower interest rate cuts. However, a potential escalation in conflicts could turn them from a factor that "limits declines" into one that "drives gains."

Gold's Long-Term Appeal During Rate Cut Cycles

In addition to its safe-haven status, gold stands out for its ability to generate long-term returns, especially during the current easing cycle initiated by major global central banks. According to WGC data, gold prices have historically provided an average return of 6% in the six months following the start of an interest rate cut cycle.

While the expectation of smaller Fed rate cuts is the primary factor pressuring gold prices in the final stretch, this reflects the unwinding of initially misplaced aggressive rate cut pricing. Therefore, as global interest rates continue to decline, this will likely become a positive factor for gold demand.

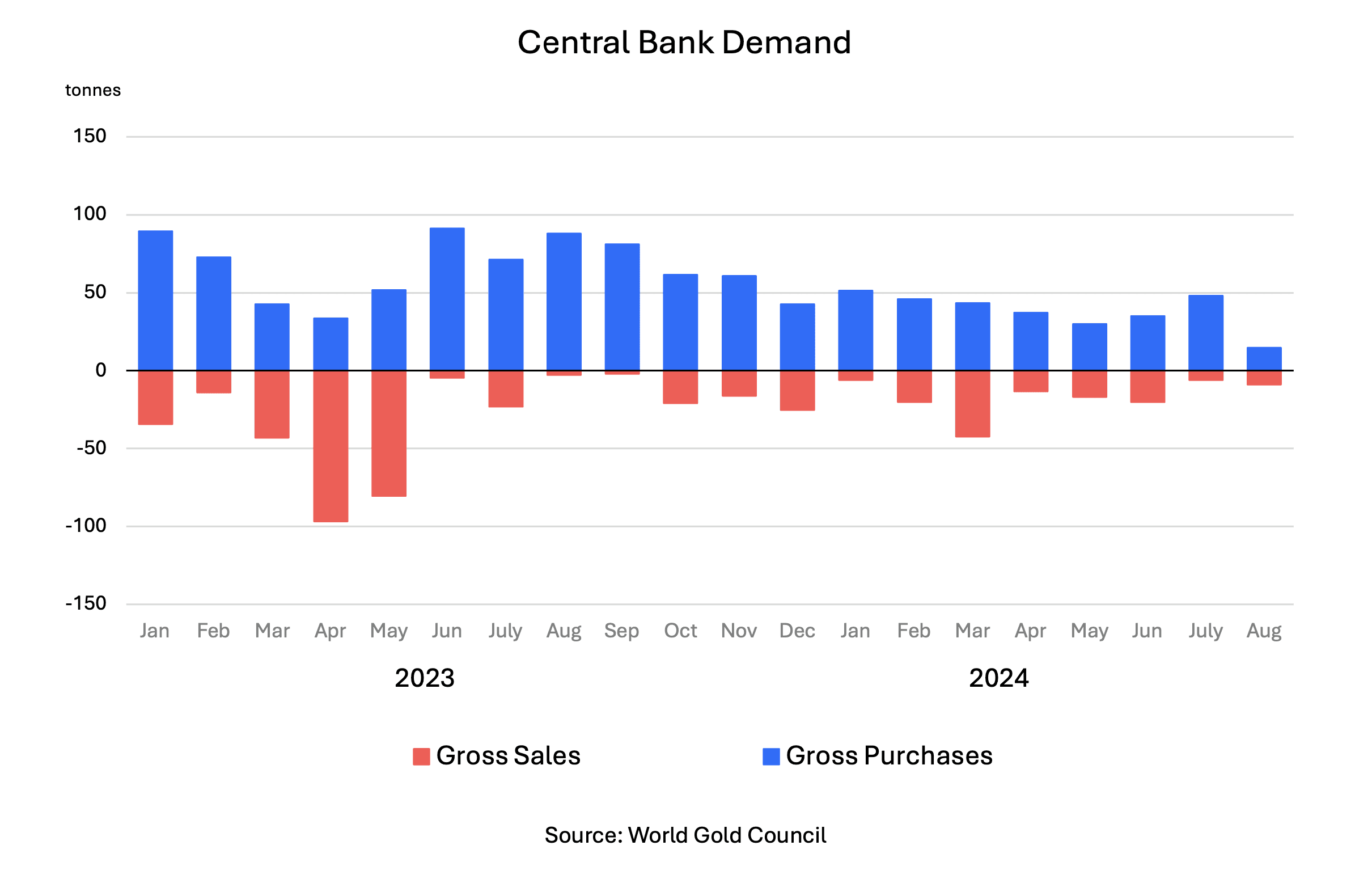

Central Bank Demand Loses Momentum

One critical factor supporting the rise in gold prices since the beginning of the year has been strong demand from central banks. In the first half of the year, central banks’ net gold purchases rose by 6% year-on-year to 183 tons. However, as of the third quarter, demand from central banks has lost momentum. Moreover, one of the major buyers, the People's Bank of China (PBoC), has completely halted its purchases.

After not reporting any gold purchases for the fifth consecutive month in August, the PBoC added 29 tons of gold to its reserves in the first four months of the year. With these purchases, it raised its gold reserves to 2,264 tons, adding 316 tons between November 2022 and April 2024, and increased the share of gold in its total reserves to 5%, the highest level since 1996. The halt in PBoC’s gold purchases leaves a significant gap in demand.

Meanwhile, net central bank gold purchases in August amounted to 8 tons, marking the lowest level since March and highlighting the loss of momentum in central bank demand.

The Central Bank of Turkey added 3 tons of gold to its reserves in August, making it the fifteenth consecutive month of net purchases. On an annual basis, it has purchased a total of 52 tons, making it the largest buyer of the year.

India’s central bank also made net purchases for the eighth consecutive month, adding 45 tons to its reserves this year, making it the second-largest buyer. Following the RBI, Poland’s central bank purchased 6 tons of gold in August, becoming the month’s largest buyer. With total purchases of 39 tons, it became the third-largest buyer of the year. In fourth place is the PBoC, which hasn’t made any purchases in the last five months.

Demand remains positive, led by emerging market central banks. However, according to WGC estimates, annual demand could fall short of last year’s. This suggests that the contribution of a key factor that drove the surge in gold prices in the first half of the year is diminishing.

Mixed Outlook for Gold Retail Demand in Asia

As gold prices have recently hit consecutive new highs, the record levels have the potential to suppress retail demand. Data from Asian markets present a mixed picture for major global buyers.

Chinese consumer demand, which accounts for about a quarter of global jewelry demand, has weakened since March. The Chinese government's recent stimulus measures have boosted optimism for economic recovery and positively contributed to gold prices. However, this optimism has started to fade due to questions about the effectiveness of the stimulus. Uncertainties surrounding the Chinese economy are acting as headwinds for the gold market.

However, persistently low consumer confidence in China significantly suppresses jewelry demand, while savings are increasing due to low expenditure tendencies. According to WGC data, some savings flow into gold bars and coins, partially offsetting the declining demand.

On the other hand, India's data shows that gold retail demand remains strong. Although the surge in gold demand, which reached record levels after gold import taxes were lowered in July, has slowed, it is expected to remain resilient due to the festival and wedding season that lasts through December.

Conclusion

In conclusion, considering the recent escalation in geopolitical tensions, the beginning of an easing cycle by major central banks, strong demand from key markets such as India, and the resilient demand from central banks, gold may maintain its positive outlook amidst changing market conditions.