IMF Spring Meetings: Global Growth Forecasts and Trade Tensions in Focus

Global economy on edge? The IMF just slashed its 2025 forecast — find out how Trump’s tariffs could reshape your financial future!

Zeynep Kucukkirali

3 Min Read

Apr 24, 2025

The International Monetary Fund (IMF), in collaboration with the World Bank, convened finance ministers and central bank governors from around the globe for its Spring Meetings in Washington. The main focus of this year’s discussions was the reassessment of the global economic outlook in light of U.S. President Donald Trump’s trade policies, which are reshaping global commerce.

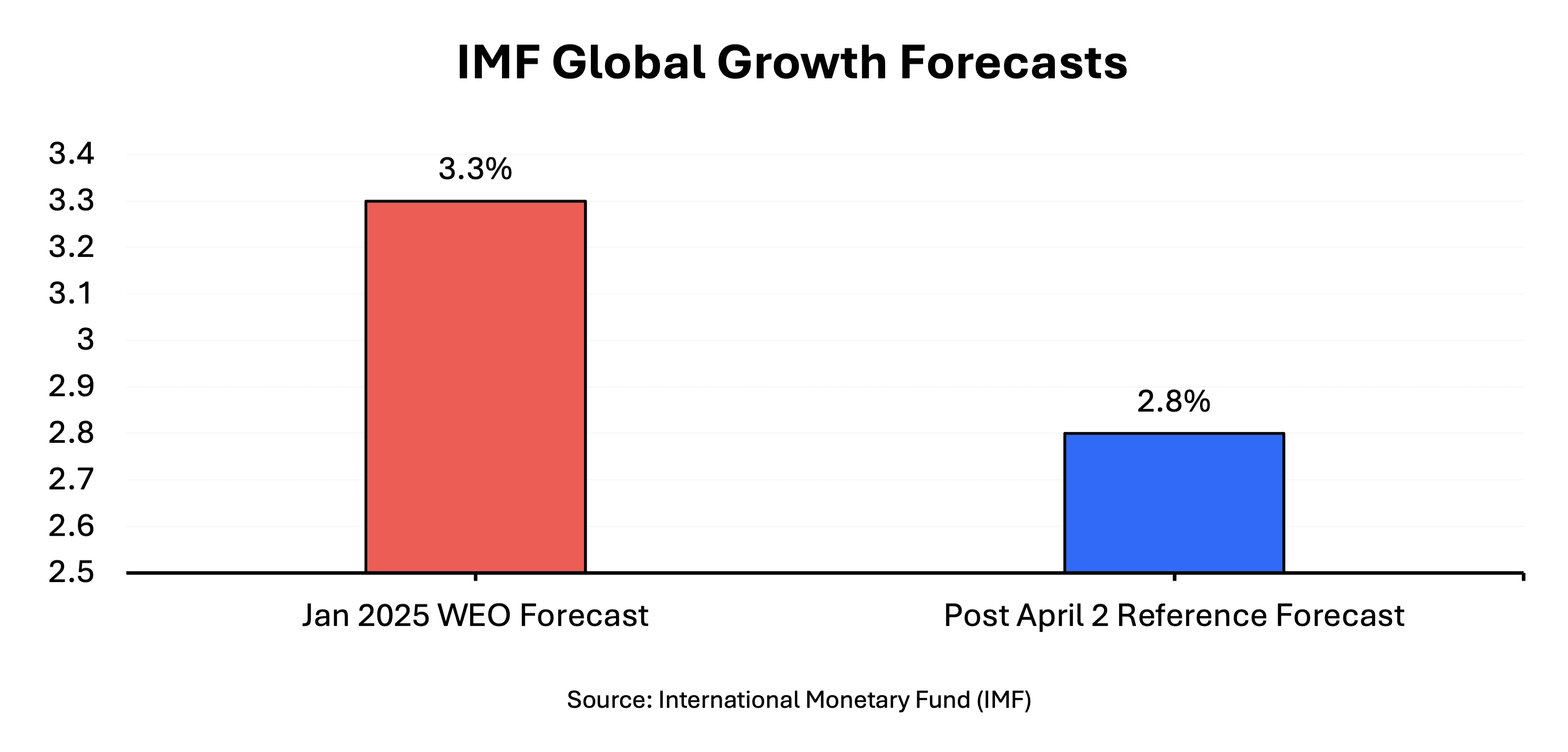

Trump’s sweeping global tariff announcements—followed by some temporary rollbacks—prompted the IMF to revise its economic forecasts due to heightened uncertainty. In its updated World Economic Outlook, the IMF lowered its 2025 global growth forecast from 3.3% in January to 2.8%, and now expects 2026 growth to come in at around 2.9%. In January, the Fund had projected 3.3% growth for both years, marking a total downward revision of approximately 0.8 percentage points.

The IMF noted that while the risk of a global slowdown has increased, a recession is not yet anticipated. However, Managing Director Kristalina Georgieva warned that persistent uncertainty surrounding a potential trade war—driven by the U.S.—could elevate recession risks. She emphasized that the level of uncertainty stemming from tariffs is “off the charts” and poses a threat to financial stability.

IMF officials added that if trade tensions are resolved more quickly, global growth projections could be revised upward, providing relief to investors and households. However, if negotiations stall and uncertainty persists, the economic impact of tariffs could become more entrenched, further weighing on global growth.

Updated Growth Forecasts by Region and Country

United States

Given President Trump’s erratic decision-making, ongoing negotiations with countries benefitting from the 90-day tariff pause, and rising tensions with China, the outlook remains clouded by uncertainty. Notably, the effective tariff rates between the world’s two largest economies far exceed the 60% level many economists believe could cripple bilateral trade—currently standing at 145% on Chinese goods and 125% on American exports.

While Trump maintains that tariffs will boost domestic manufacturing and economic growth, economists strongly disagree. Demand in the U.S. had already weakened since the start of the year due to uncertainty surrounding trade policy. Tariffs announced on April 2—and subsequently paused or revised—have further deteriorated expectations.

The IMF lowered its 2025 U.S. growth forecast to 1.8%, down 0.9 points from January, with tariffs accounting for 0.4 percentage points of that decline. Inflation expectations were also revised upward by nearly 1 percentage point to 3% from 2%.

China

For trading partners, tariffs typically represent a negative demand shock, discouraging foreign buyers and triggering deflationary pressure, even if some countries benefit from trade diversion.

Given the scale of trade between China and the U.S., and consistent with this deflationary impulse, the IMF cut China’s growth forecast for 2025 and 2026 to 4%, a downward revision of 0.6 and 0.5 percentage points, respectively.

The IMF’s downward revision for China was smaller than for the U.S. due to recent data showing a sharper decline in Chinese imports from the U.S., while U.S. demand for Chinese imports remained relatively strong. Economists expect U.S. exports to China to fall quickly, while the drop in Chinese exports to the U.S. may occur more gradually.

Japan

Like many countries, Japan received a 90-day deferral from Trump’s so-called reciprocal tariffs, which were initially set at 24%. However, a 10% baseline tariff remains in place, along with 25% duties on automobiles, steel, and aluminum.

Against this backdrop, The IMF downgraded Japan’s 2025 growth forecast by 0.5 percentage points to 0.6%. Roughly 0.28 percentage points of that decline are attributed directly to tariffs, with the remainder linked to secondary effects and rising uncertainty. Nearly half of the direct impact stems from the auto sector, which accounts for 40% of Japan’s exports to the U.S.

Eurozone

As a major U.S. trading partner, the eurozone is also vulnerable to both reciprocal and sector-specific tariffs. The outcome of ongoing negotiations remains unclear, but sources suggest the U.S. will not lift all tariffs on the EU. This could further dampen already subdued economic activity across the bloc.

Still, the U.S. is applying relatively lower tariffs on the eurozone. Reflecting this, the IMF lowered its growth forecast for the region by 0.2 percentage points to 0.8%. Stronger fiscal support in 2025 and 2026 is expected to provide some offsetting relief.

United Kingdom

The IMF downgraded the UK’s growth outlook more sharply than for other major European economies. Despite facing only a 10% baseline tariff, the UK is projected to be more severely affected in 2025 and 2026.

Germany, France, Italy, and Spain—which faced 20% tariffs before the 90-day suspension—received smaller downward revisions. Still, the UK is expected to outperform these peers, growing 1.1% in 2025 and 1.4% in 2026.

Emerging Markets

Many emerging market economies are at risk of significant slowdowns depending on how tariffs are structured and implemented. The IMF cut its 2025 growth forecast for the emerging markets group by 0.5 percentage points to 3.7%.

In Conclusion: Global Outlook Hinges on Trump’s Tariff Path

Ultimately, the trajectory of global economic activity will hinge largely on President Trump’s final decisions regarding tariffs. If a clear resolution is delayed, prolonged uncertainty could continue to weigh on investment, consumer sentiment, and trade flows across both advanced and emerging economies. As Duhani Capital Research, we assess that until greater clarity emerges, the global outlook will likely remain fragile, with downside risks persisting.