Inflation Report Looms and Fed in the Spotlight: Will CPI Data Reinforce Rate Cut Bets?

Trump's policies spark inflation concerns as CPI data looms - will the Fed be forced to cut rates sooner than expected?

Zeynep Kucukkirali

4 Min Read

Mar 11, 2025

As the U.S. economy grapples with uncertainties stemming from the new administration's policies, recent weak economic data has cast doubt on U.S. economic exceptionalism and heightened concerns about the outlook. The data indicates a slowdown in economic activity, declining consumer and business confidence, a softening labor market, and inflation expectations surging to multi-decade highs.

Donald Trump's tariff, tax, and immigration policies are expected to add upward pressure on prices while weighing on economic growth in the coming period. Such a scenario could push the economy toward stagflation, placing the Federal Reserve in a difficult position.

President Trump, however, downplayed concerns over a slowdown, arguing that the economy is in a transition phase and that focusing on early results has contributed to market volatility.

Meanwhile, Fed officials acknowledge the risks but maintain an optimistic outlook on the economy. In recent statements, policymakers have reiterated that they need to see "meaningful progress" on inflation before considering any policy adjustments. However, a weakening labor market could force them to cut rates, as noted by Fed Chair Jerome Powell.

Markets have shifted their focus from inflation fears—heightened after Trump's election victory—to growth risks. Despite the Fed's cautious stance, futures markets indicate that traders are betting on three-quarters of a percentage point in rate cuts this year. Still, uncertainties remain high, and traders are awaiting further data for more clarity.

February CPI Report in Focus: Will Inflation Continue to Ease or Prove More Persistent?

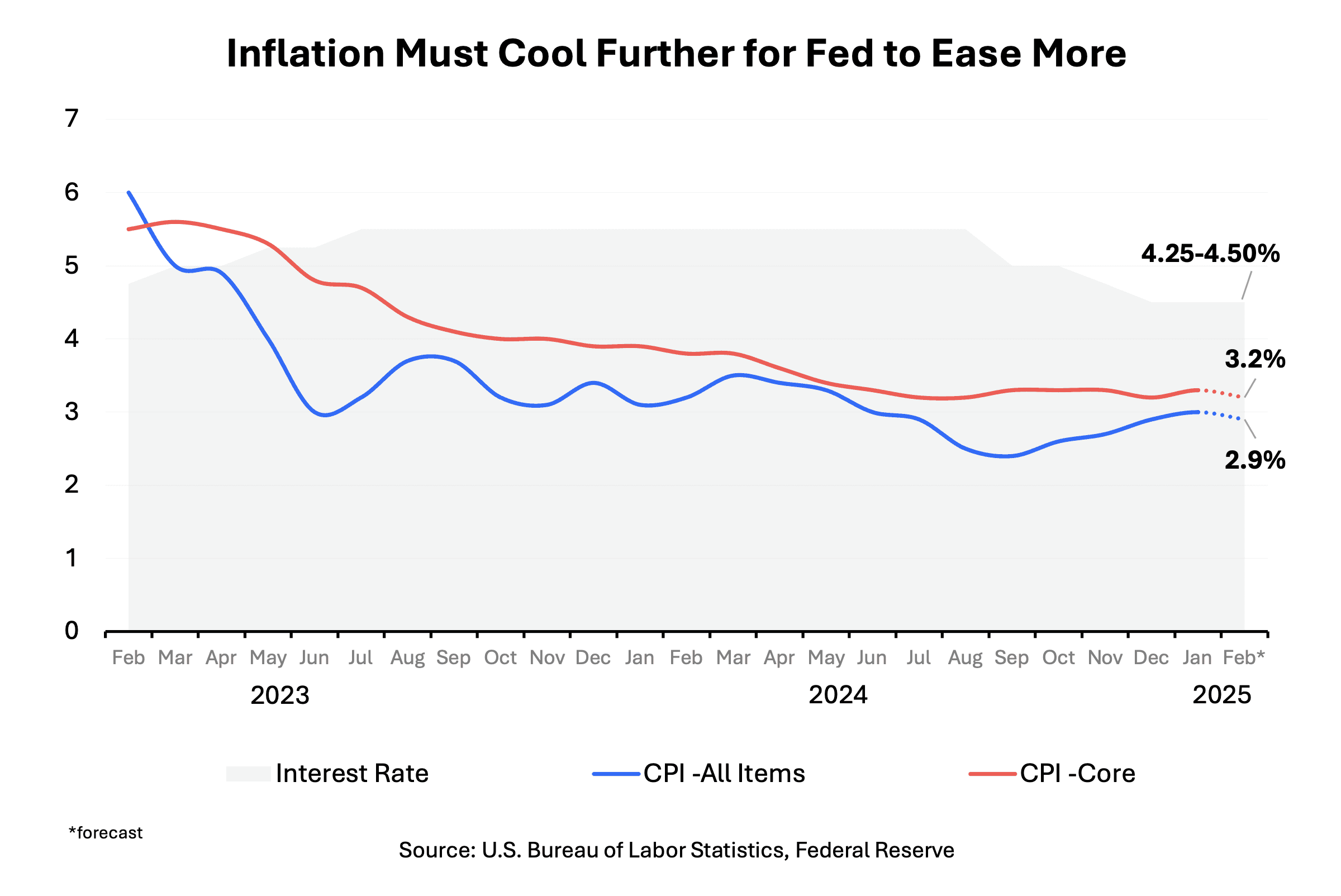

In January, the consumer price index (CPI) significantly exceeded expectations. The so-called core measure, which excludes volatile food and energy, accelerated at a monthly rate of 0.4%, doubling the previous month's increase. On an annual basis, it rose 3.3%, defying expectations of a slowdown.

The data suggests mounting price pressures in the U.S. at the start of the year. However, economists attributed these increases to one-time price adjustments typical at the beginning of the year, rather than a broad acceleration in inflation. This consensus helped alleviate inflation concerns.

The February CPI report, set to be released on Wednesday, is expected to further ease worries about rising inflation. However, the effects of early-year price adjustments have likely carried over into this report, leading to a modest recovery.

According to a Bloomberg survey, economists predict that the core CPI slowed to 0.3% month-over-month, bringing the annual rate to 3.2%. The headline index is expected to increase 2.9% year-over-year.

In such a scenario, this would indicate that inflation remains well above the Fed's 2% target but continues to make progress toward the target, albeit at a slow pace.

As Duhani Capital Research team, we believe that a report like this would help ease inflation concerns and keep market focus on growth risks. This would likely sustain pressure on the U.S. dollar, and for dollar bulls to regain momentum, a shift in this narrative would be necessary—driven by stronger economic data or developments.

Consumers Expect Higher Prices and Weaker Job Market: What It Means for the Fed

Meanwhile, U.S. consumers expect higher inflation in the near term and are growing more pessimistic about their financial outlook.

The New York Fed's consumer expectations survey showed that one-year inflation expectations rose from 3.0% in January to 3.1% in February. American consumers now anticipate faster price increases for gasoline, food, medical care, and rent.

At the same time, consumer expectations regarding unemployment, default risk, and credit access have notably worsened. The probability of missing a minimum debt payment over the next three months has surged to its highest level since April 2020, while the percentage of respondents expecting their financial situation to worsen in the next year is at a 15-month high.

Job expectations also reflect growing pessimism. U.S. households now see their chances of finding a new job within three months at their lowest level in a year, while the percentage of those expecting the unemployment rate to rise is at its highest since September 2023.

The deterioration in short-term consumer expectations is fueled by uncertainty surrounding Trump's economic policies. The rise in inflation expectations is particularly concerning, as such expectations can become a self-fulfilling prophecy, ultimately pushing actual inflation higher. Notably, following Trump's election victory, expectations of higher tariffs and faster inflation prompted consumers to stockpile durable goods, pulling demand forward.

For this reason, inflation expectations are closely monitored by the Fed, as persistent increases in expectations can influence policy decisions. However, while short-term inflation expectations have risen, three- and five-year expectations remain anchored at 3%, offering some reassurance to Fed officials. Policymakers have previously indicated that if long-term inflation expectations remain stable, tariff-driven price increases may not significantly impact monetary policy decisions.

Fed officials will meet on March 18-19 to assess the state of monetary policy. No rate adjustments are expected at this meeting, but updated economic projections will be released, which will be crucial for shaping market expectations.