Market in Focus: Confidence Cracks, Central Banks Caught in the Middle

Why are investors rushing to safe assets? Discover how trade tensions and Fed drama are changing the market game.

Zeynep Kucukkirali

8 Min Read

Apr 22, 2025

Global markets reel as Trump's tariff flip-flops fuel volatility. Gold surges past $3,495/oz while S&P 500 tumbles 4.42%. Fed independence questions mount amid Powell criticism. ECB cuts rates for the seventh time since June as Europe braces for trade impact. China posts strong Q1 GDP, but analysts warn of pre-tariff stockpiling effects.

Key Market Takeaways

Tariff Confusion Fuels Global Volatility

Markets remain on edge as President Trump continues to oscillate between tariff suspensions and new investigations. While the 90-day pause on reciprocal tariffs offered some relief, tensions with China worsened, and new probes into semiconductors and pharmaceuticals opened fresh fronts of uncertainty.

Fed Policy in the Crosshairs

Speculation over the Fed's independence intensified after Trump's remarks targeting Chair Powell. Although policymakers continue to emphasize inflation risks, markets now price in over three cuts this year—starting as early as June.

Safe-Haven Demand Accelerates

Gold surged past $3,495/oz, hitting new record highs. The yen and Swiss franc strengthened amid flight-to-safety flows, while U.S. equities tumbled and Treasuries slipped.

Data Divergence Clouds Outlook

U.S. retail sales surprised to the upside, while manufacturing surveys signaled weakness. China posted stronger-than-expected Q1 GDP, but analysts caution against reading too much into pre-tariff stockpiling.

Europe and Asia Adjust to Trade Shock

The ECB delivered its seventh rate cut since last June, while the BoJ and RBA held steady. The UK faced its fastest pace of layoffs since the pandemic, and Australian job growth fell short of expectations.

This Week in Numbers

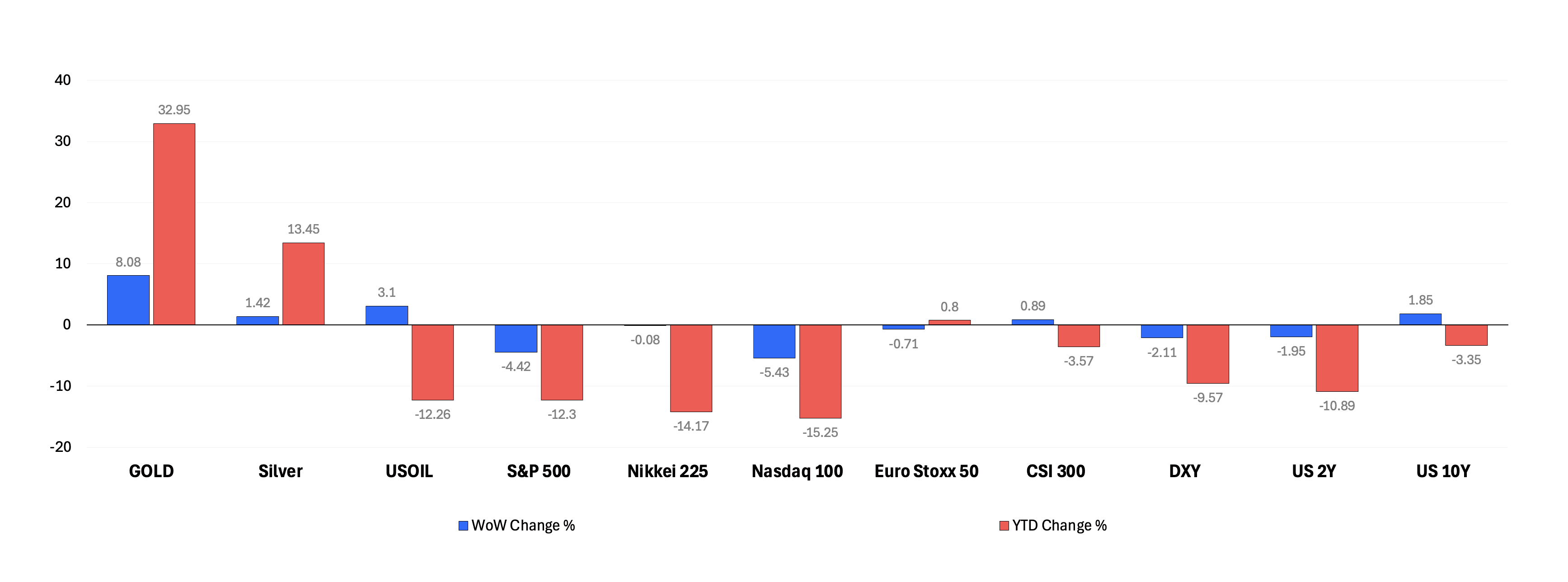

Tariffs, uncertainty, and Trump’s back-and-forth remarks are causing investors to question the safe-haven status of U.S. assets. This week:

The dollar declined by 2.11% against major peers

U.S. Treasury yields diverged

Equity markets extended their declines:

S&P 500 lost 4.42%

Nasdaq fell 5.43%

Japan and Europe down; China’s CSI 300 up 0.89%

Meanwhile, demand for safe-haven assets remains robust:

Gold has gained nearly 33% year-to-date

Jumped nearly 8% last week alone

Hit a new record above $3,495 per ounce

Flows into the Japanese yen and Swiss franc have also stayed strong.

Across the Globe: Last Week

U.S. Recap – Policy Uncertainty Weighs on Sentiment

Markets continued to grapple with growing policy uncertainty as President Trump escalated tariff threats while openly challenging the independence of the Federal Reserve. Although March retail sales surprised to the upside with a 1.4% gain—driven largely by pre-tariff auto purchases—industrial production declined 0.3% on the month, and New York manufacturing activity contracted for the second consecutive month, signaling persistent weakness in the real economy.

Inflation expectations added another layer of concern. The New York Fed’s survey showed one-year inflation expectations rising to 3.6%, while longer-term expectations remained unchanged. Separately, the University of Michigan’s survey showed long-term inflation expectations holding at an elevated 4.4%. The perceived risk of rising unemployment also climbed. Combined with tariff-driven cost pressures, these developments are complicating the Fed’s ability to balance its dual mandate.

Fed Chair Jerome Powell emphasized that price stability remains the foundation for sustained employment gains. While markets continue to price in at least three rate cuts this year—starting as early as June—Fed officials have signaled a more cautious approach. Powell and others reiterated that further clarity on inflation and trade outcomes is needed before adjusting policy.

Adding to the tension, Trump’s repeated attacks on Powell and suggestions that he could be removed rattled investor confidence. The dollar slipped to a multi-year low, equities pulled back, and the Treasury yield curve steepened. For now, the Fed appears inclined to stay on hold through midyear, with one or two rate cuts possible in the second half depending on incoming data.

Europe in Focus – Pressure Mounts Amid Tariffs & Weak Growth

Eurozone

The European Central Bank cut rates for a seventh time since June of last year, lowering the deposit rate from 2.5% to 2.25%. With U.S. trade tensions weighing on the region’s recovery, markets are anticipating further easing.

President Christine Lagarde acknowledged that the economic effects of tariffs would take time to materialize and warned of rising downside risks to growth. Policymakers also removed the term "restrictive" from their policy statement.

The Euro Area is now facing 10% tariffs under the 90-day pause imposed by the U.S., down from an earlier 20% proposal, while also grappling with 25% duties on autos, steel, and aluminum. Negotiation outcomes remain uncertain, but some sources say the U.S. does not plan to lift most tariffs on the bloc.

Core inflation rose 2.4% in March, close to the ECB's target. However, falling energy prices – driven by expectations of weakening global trade – may push inflation below target in the coming months.

As tariffs begin to hit trade activity, economic output is also expected to contract. Economists forecast further ECB rate cuts in June and September, with the possibility of more depending on incoming data.

As the region’s largest economy, Germany is feeling the brunt of tariff-related uncertainty most acutely. Investor confidence has declined sharply, with economic sentiment in April falling to its lowest level since 2022. Optimism fueled by government spending quickly reversed as President Trump’s trade stance took center stage. Tariffs on automobiles, in particular, are weighing heavily on expectations for the country’s economic outlook. According to a recent survey, one in three companies is now considering layoffs this year due to growing pessimism.

UK

Layoffs in the UK accelerated to the fastest pace since the start of the pandemic, driven by U.S. tariffs and April payroll tax hikes totaling $34.3 billion. In March, payroll employment fell by 78,467, and job vacancies in Q1 dropped below pre-pandemic levels for the first time since 2021. The data signal mounting pressure on employers from rising labor costs and global uncertainty.

Meanwhile, headline inflation eased for a second straight month in April ahead of tax increases. CPI rose 2.6% year-over-year, down from 2.8%, while core inflation slipped from 3.5% to 3.4%.

Still, tax increases that took effect in early April are expected to raise household expenses by an average of £600, likely pushing headline inflation above 3% in the near term.

The Bank of England faces a policy dilemma: balancing tax- and tariff-driven inflation against the need to support growth. Traders are pricing in three quarter-point rate cuts this year, beginning in May.

Asia Watch – Growth Divergence, Inflation Surprises

China

China's economy delivered a surprising show of strength in early 2025, boosted by consumer subsidies and a surge in export shipments aimed at front-running new tariffs. GDP rose 5.4% year-over-year in Q1, exceeding forecasts of 5.2%. Much of the momentum came from a sharp acceleration in March, as companies rushed to ship goods before additional tariffs took effect.

Both production and consumption showed unexpected strength in March. Industrial production jumped 7.7% from the previous month, while retail sales rose 5.9%.

However, analysts remain cautious. The ongoing trade standoff with the U.S. casts doubt on whether this growth can be sustained in the coming quarters. Many believe China’s full-year performance will depend heavily on the scale and speed of policy support from Beijing.

Despite expectations for easing at the April 20 PBoC meeting—either via a rate cut or a reserve requirement adjustment—the central bank took no action. In the meantime, the government expanded spending at the fastest Q1 pace since 2022 and introduced new support programs for exporters through the Ministry of Commerce.

Japan

Consumer inflation accelerated in March. The core CPI, which excludes fresh food, rose 3.2% year-over-year, up from 3% previously. Excluding energy as well, the index climbed 2.9% – the fastest pace since March 2024.

The surge was driven primarily by rice prices, which rose over 92% from a year earlier – the sharpest increase since 1971. This reinforces the role of food inflation as the main driver of inflation in Japan.

Inflation has remained above the Bank of Japan’s 2% target for three years, following more than a decade of deflation. Consumer confidence has fallen to a two-year low, and household inflation expectations have picked up.

This backdrop supports the BoJ’s current tightening path. However, policymakers may remain cautious as they assess the economic fallout from U.S. tariff negotiations. Economists expect the first rate hike in July.

Australia

Australia’s labor market showed signs of softening in March. The unemployment rate rose from 4.0% to 4.1% – below the 4.2% forecast – while employment increased by just 32,000, missing the 40,000 estimate. Slightly more than half of the job gains came from part-time positions.

While the data suggest the labor market remained resilient before the imposition of U.S. tariffs, this could change as trade measures begin to bite. A 10% tariff on Australian goods directly affects about 5% of its exports.

Of greater concern is the broader impact of U.S.-China trade tensions. China accounts for roughly one-third of Australian exports, and any slowdown in Chinese demand could spill over into Australia.

Traders are now pricing in four rate cuts from the Reserve Bank of Australia this year. However, following the employment report, the odds of a May cut declined. The RBA held rates steady at 4.1% at its early-April meeting.

Market Calendar: What to Watch This Week

U.S.

Markets will focus on flash PMIs for both manufacturing and services, offering fresh insights into the pace of economic activity across sectors. The Federal Reserve’s Beige Book—set for release midweek—will provide anecdotal evidence on regional business conditions, labor markets, and price dynamics.

Additionally, the University of Michigan’s updated sentiment and inflation expectations surveys will be in focus. Last month, long-term inflation expectations climbed to 4.4%; whether they remain anchored will be critical for shaping Fed policy expectations.

Europe

In the euro area, the preliminary consumer confidence index will be watched closely following last month’s decline, particularly as new U.S. tariffs begin to take effect. Flash PMI readings across the bloc and in Germany will also be key for gauging how trade disruptions are affecting business activity.

In the UK, PMI data will offer a real-time snapshot of manufacturing conditions, while March retail sales will help assess how consumers responded ahead of the April payroll tax increases and tariff adjustments.

Asia

Following last week’s national CPI data, attention will turn to Japan’s Tokyo consumer price index for April. The core measure, which excludes fresh food, is expected to rise 3.2% year-over-year—up sharply from 2.4%—likely reflecting a surge in rice prices. The reading could reinforce expectations for a BoJ rate hike later this year.

Dive into the complete analysis ➡️ short.duhani-campaign.com/ilHvyr

Investors face mounting uncertainty as trade tensions and policy unpredictability dominate market sentiment. With safe-haven assets rallying and central banks recalibrating their approaches, vigilance and strategic positioning remain essential in navigating these turbulent market conditions.