Strong Start, Fragile Future: Trump's Trade Moves Cloud Outlook

Explore how Trump’s trade tariffs are impacting U.S. economic growth, manufacturing, and consumer spending!

Zeynep Kucukkirali

3 Min Read

Apr 17, 2025

Trump’s tariff policies gave the U.S. economy a strong start in Q1, with rising manufacturing and consumer spending. But uncertainty looms as trade tensions, investment delays, and price hikes threaten future growth and market confidence.

Resilient Now, Unclear Ahead: U.S. Data Collides with Trade Uncertainty

As President Donald Trump’s tariff policies and unpredictable statements continue to send shockwaves through global trade channels, economic data from the first quarter of the U.S. economy paint a mixed picture. While both manufacturing output and consumer spending came in stronger than expected in March, mounting price pressures and deteriorating sentiment are raising questions over the sustainability of growth.

According to data released by the Federal Reserve on Wednesday, manufacturing output rose by 0.3% in March following an upwardly revised 1% increase in February—beating the consensus forecast of 0.2%. Gains in motor vehicle production supported the headline figure. However, overall industrial production declined by 0.3% during the same period, marking its first drop in four months.

The manufacturing sector posted a strong 5.1% gain in the first quarter—its largest quarterly increase since late 2021—buoyed by rising orders ahead of the implementation of new tariffs. Still, concerns remain about whether this momentum can be sustained, as Trump’s high tariffs on Chinese imports and erratic policy shifts have injected fresh uncertainty into the sector.

While several manufacturers have announced plans to expand production in the U.S., the lack of clarity in bilateral trade agreements is prompting many to delay investment decisions. This policy gray zone created by tariffs is affecting not only production but also retail sales and consumer behavior.

Consumer Spending Accelerates, but Sustainability in Question

Alongside the rise in manufacturing output, government data released Thursday showed that consumer spending also picked up sharply at the end of Q1.

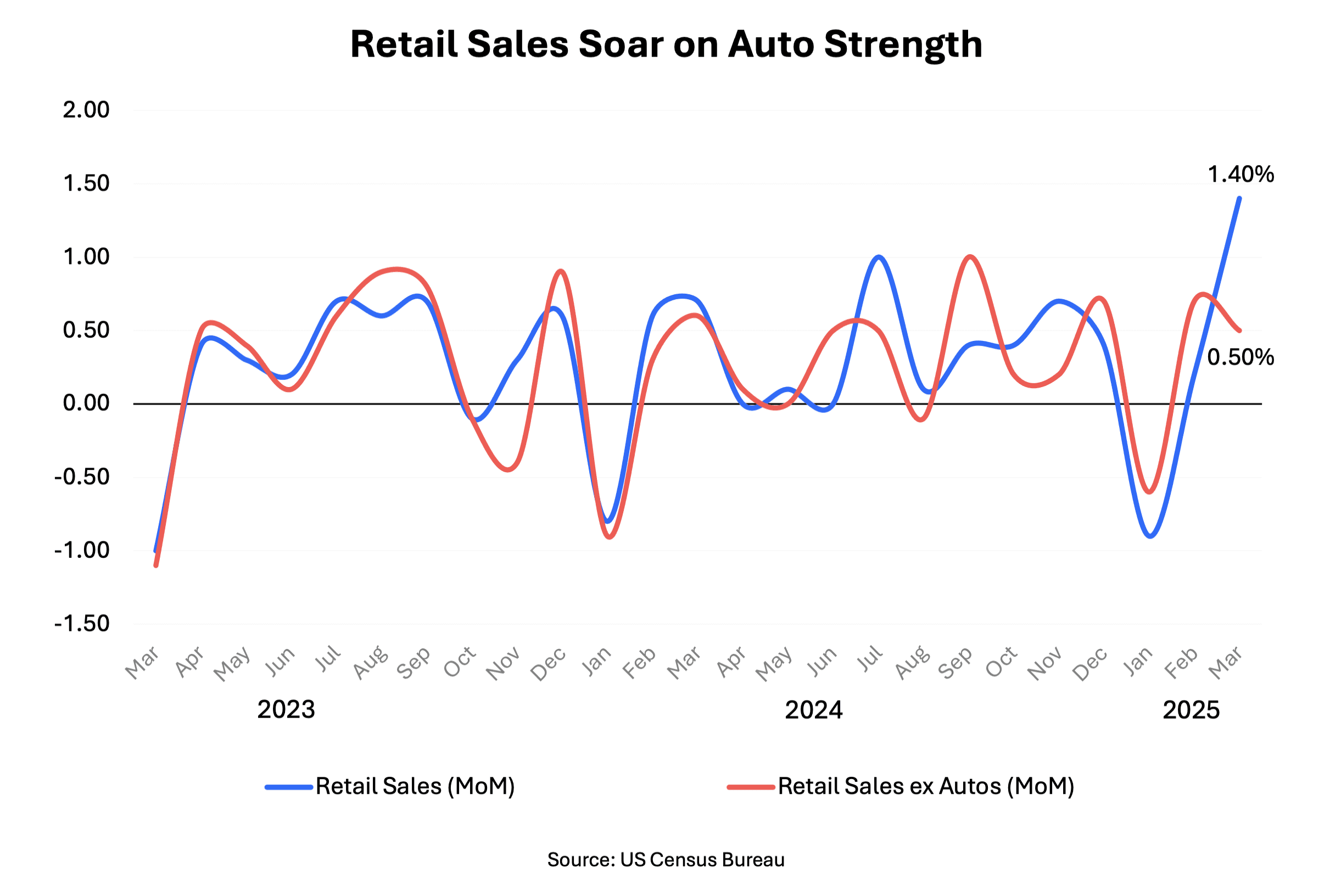

Retail sales rose 1.4% in March from the previous month (prior: +0.2%), marking the fastest monthly increase since early 2023. On a year-over-year basis, growth jumped to 4.6% from 3.5%.

This surge in spending likely reflects a rush by consumers to make large purchases—such as automobiles, electronics, and home appliances—before tariffs push prices higher. Increases were especially notable in categories like building materials, sporting goods, and electronics, most of which are typically imported from China. However, the biggest driver was autos; excluding motor vehicles, retail sales rose by just 0.5%.

Amid efforts to avoid the 25% tariff on imported finished vehicles, auto purchases surged by 5.3%—the fastest pace in nearly four years. Honda Motor Co. posted a 13% increase across its brands, while Ford Motor Co.’s retail sales rose by 19%.

The 25% tariff on imported autos will add significant costs to vehicle production, most of which will be passed on to consumers. According to a recent report by Anderson Economic Group, new tariffs could raise costs by at least $2,500 per vehicle in the entry-level segment, and as much as $20,000 for luxury ones.

Some automakers have tried to ease customer concerns—Hyundai pledged to keep prices steady through June 2. However, Ford Motor Co. announced it is preparing to raise prices on cars coming off the production line next month—unless President Trump delivers on the tariff relief he hinted at—with current inventory prices remaining unchanged.

Sentiment Deteriorates, Outlook Weakens

While the tariff threat has provided a temporary boost to some retailers, uncertainty surrounding negotiations—and the possibility of a trade war with China—is causing businesses to freeze hiring and investment. Both consumers and businesses report being shaken by the back-and-forth policy changes, unable to plan ahead or act with confidence. Notably, consumer confidence remains near its lowest level in data going back to the 1950s.

Beyond elevated tariffs, the deterioration in sentiment is exerting further pressure on the economy. As a result, economists have increased the probability that the U.S. could enter a recession. Still, for now, the labor market remains strong, wages are rising, and inflation remains relatively flat—factors that have helped support robust pre-tariff spending.

The sharp rise in consumer spending during the final month of the quarter has also pushed Q1 GDP forecasts higher. According to the Atlanta Fed’s latest GDPNow estimate, growth is now projected at -0.1%, a notable improvement from the previously expected -0.5% contraction—excluding the distorting effects of gold imports.

However, as Duhani Capital Research team, we assess that as tariffs begin to pass through more clearly to consumer prices in the coming period, a slowdown in spending may emerge, potentially putting additional pressure on economic growth.

Investors, likewise, appear increasingly aware of the potential for tariffs to weigh on U.S. economic growth. Despite the stronger-than-expected data, markets showed little optimism in response.

Trade Hopes Thin, Safe-Haven Bets Stay Strong

Against this backdrop, how trade talks evolve during Trump’s 90-day tariff truce will be critical. Successful negotiations could help restore sentiment and ease pressure on growth and inflation.

Still, for a meaningful rebound in risk appetite, markets will likely need greater clarity on the direction of talks. In the meantime, demand for safe-haven assets is expected to remain strong, with upward pressure on gold and similar instruments likely to persist.