Week Ahead: Trade Policy, Interest Rates, and Market Reactions

Explore the 'Week Ahead' as trade policy shifts, interest rates hold, and markets react. Stay informed with 'Week Ahead' insights on global trends.

Zeynep Kucukkirali

4 Min Read

Feb 10, 2025

Global markets brace for a pivotal week amid U.S. President Trump's new tariff announcements and Federal Reserve Chair Powell's testimony. Key focus remains on Wednesday's U.S. inflation data, following strong wage growth in January's jobs report. Gold hits record highs above $2,895/oz as safe-haven demand surges, while the dollar strengthens on expectations of sustained high rates.

Key Events and Data to Watch This Week

Tuesday

UK Like-for-Like Retail Sales (Jan)

Wednesday

US Consumer Price Index (Jan)

Thursday

Japan Producer Price Index (Jan)

Australia Consumer Inflation Expectations (Feb)

Germany Consumer Price Index (Jan)

UK Gross Domestic Product (Q4) Preliminary

UK Industrial Production (Dec)

Eurozone Industrial Production (Dec)

US Producer Price Index (Jan)

Friday (18:00)

Eurozone Employment Change (Q4) Preliminary

Eurozone Gross Domestic Product (Q4) Preliminary

US Retail Sales (Jan)

US Industrial Production (Jan)

Markets on Edge: Tariffs, Inflation, and the Fed's Next Move

This week is relatively quiet in terms of the economic calendar, but traders will still be closely monitoring key data releases and developments. On one hand, they will be watching for updates on the tariffs that U.S. President Donald Trump said he plans to announce on Monday.

On the other hand, they will focus on Federal Reserve Chair Jerome Powell’s testimony, January’s U.S. inflation data, and other important economic reports from various countries, including inflation, retail sales, growth, and production figures, in an effort to assess the global economic outlook.

The jobs report released on Friday showed that U.S. payrolls slowed but continued to expand at a solid pace, while unemployment declined and wages grew faster than expected. In January, nonfarm payrolls increased by 143,000—lower than the median economist forecast of 170,000. However, the unemployment rate fell from the previous 4.1% to 4%.

Meanwhile, payroll gains for the previous two months were revised upward by a total of 100,000. November’s payrolls were revised up from 212,000 to 261,000, while December’s figures were increased from 256,000 to 307,000.

Additionally, the annual revisions were not as deep as previously estimated. According to preliminary estimates from August, payroll gains for the 12 months through March 2024 were expected to be revised downward by 818,000, but the final adjustment was limited to 589,000. After the latest revisions, the average monthly job gains for 2024 stood at 166,000, down from the initially reported 186,000.

The U.S. Bureau of Labor Statistics stated that the wildfires in Los Angeles and adverse weather conditions in other regions had no noticeable impact on employment throughout the month.

Meanwhile, the average hourly earnings for all employees on nonfarm payrolls rose by 0.5% in January, significantly exceeding the 0.3% forecast. Over the past 12 months, average hourly earnings increased from 3.9% to 4.1%, while expectations had been for a decline to 3.8%.

As a result, the jobs report reinforced the narrative that the U.S. labor market remains largely stable and healthy. Moreover, the continued strong pace of wage growth suggests that the labor market remains a source of inflationary pressure. This, in turn, justifies the Federal Reserve’s stance of keeping interest rates steady for the foreseeable future, especially amid the uncertainty caused by Trump’s policies.

Additional support for the Fed’s cautious stance came from another report released on Friday. The University of Michigan’s survey indicated that consumers expect prices to rise much faster over the next year due to Trump’s tariff policies, causing consumer confidence to fall to its lowest level in seven months.

U.S. consumers now anticipate inflation to increase by 4.3% over the next year, up by one percentage point from the previous month’s expectation. They also predict that inflation will average 3.3% over the next five to ten years.

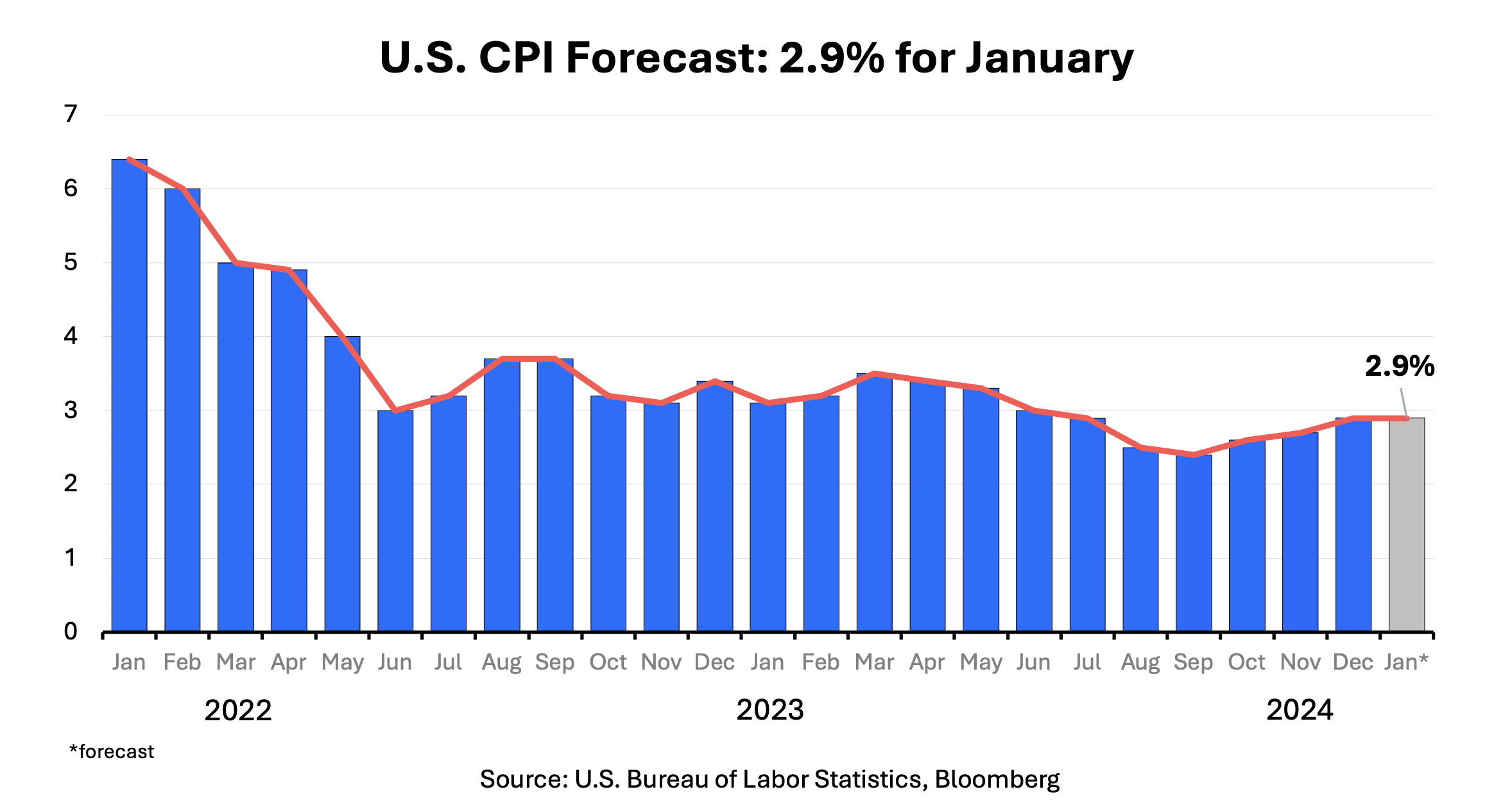

For further insights into U.S. inflation, the Consumer Price Index (CPI) for January, set to be released on Wednesday, will be closely watched. The median economist forecast suggests that the so-called core CPI, which excludes food and energy costs, is expected to rise by 0.3% for the fifth time in the past six months, with the annual increase projected at 3.1%.

Meanwhile, overall prices for all items likely rose 2.9% compared to the same period last year, which would confirm that progress toward the inflation target has stalled.

As the U.S. economy continues to perform strongly and the labor market remains resilient, persistently high inflation supports expectations that the Fed will keep rates unchanged for an extended period. Swap traders are now pricing in the likelihood that the Fed will remain on hold until at least September, which continues to provide support for the U.S. dollar.

On the other hand, Donald Trump announced on Monday that he would impose a 25% tariff on all steel and aluminum imports—applicable to all countries. He also stated that later in the week he would introduce additional tariffs against nations that impose taxes on U.S. imports.

Trump continues to make new decisions regarding tariffs, highlighting the ongoing risk that these trade duties could gradually increase over time. This risk raises concerns about inflation in the U.S., reinforcing the likelihood that the Fed will be prevented from cutting interest rates while also supporting a stronger dollar.

Some Wall Street bank strategists argue that even the mere consideration of Trump’s tariff threats could continue to drive the dollar higher. The dollar is expected to break parity against the euro, while other currencies are likely to depreciate against it.

Conversely, some strategists believe that Trump is using tariffs as a negotiating tool.

While they acknowledge that there are valid arguments for a stronger dollar, they do not anticipate an escalation of a trade war and, therefore, do not expect the dollar to strengthen as much as others predict. Additionally, some analysts argue that U.S. employment figures are overstated and are betting that the Fed will continue to ease policy gradually this year.

An analysis of the latest data from the Commodity Futures Trading Commission (CFTC) as of February 4 shows that speculative traders currently hold approximately $31.2 billion in long dollar positions. This marks a decline of more than $2 billion from the previous week.

However, it is evident that traders remain committed to their bullish dollar bets until more clarity emerges regarding Trump’s policies and their potential consequences. For these bets to reverse, developments that alleviate concerns about tariffs and inflation will be necessary.

As a result, Trump’s actions this week and the inflation report will serve as crucial catalysts. Additionally, Federal Reserve Chair Jerome Powell’s semiannual testimony before lawmakers on Tuesday and Wednesday will be closely watched. Powell is likely to emphasize the resilience of the economy as the main reason for the Fed’s reluctance to lower interest rates quickly, and his comments could contribute to market volatility.

Gold on Fire: Safe-Haven Demand Pushes Prices to New Highs

Gold continues to benefit from rising global uncertainties. Donald Trump’s latest tariff threats have further fueled the flight to safe-haven assets, pushing gold above $2,895 per ounce and marking a new all-time high.

Despite high interest rates, U.S. economic data continues to show resilience, suggesting that the neutral rate—the level that neither slows nor stimulates the economy—may be higher than previously estimated, Minneapolis Fed President Neel Kashkari said on Friday

This implies that the Fed may have less room for rate cuts. In theory, higher interest rates are a negative factor for gold, which does not yield interest. However, its role as a store of value in uncertain times continues to shine, even in the face of elevated rates and a strong U.S. dollar. Meanwhile, central banks are also increasing their gold reserves amid ongoing global uncertainties.

With gold prices just a step away from the $3,000 mark, the metal is likely to continue benefiting from Trump's tariff rhetoric and uncertainty surrounding the global economic outlook. However, historically high prices are making gold more expensive for foreign buyers, which could put pressure on demand and slow its upward momentum.

Traders will keep a close eye on this week’s key developments to shape their expectations for gold prices.