Weekly Economic Roundup: U.S.-China Standoff, EU Talks, and Investor Flight to Safety

Trump’s tariff games shake markets, rattle the Fed, and fuel gold’s rise. What’s next for the global economy? Stay ahead with key insights!

Zeynep Kucukkirali

4 Min Read

Apr 18, 2025

The Trump administration’s back-and-forth tariff actions and ambiguous negotiations with allies continue to pressure the global economic outlook. Additional steps against China, strained talks with Europe, and political rhetoric targeting the Fed are all contributing to mounting uncertainty, further eroding confidence in the U.S. economy.

Trade Talks in Limbo: Allies Pressured, Outcomes Unclear

Markets are closely monitoring how trade talks evolve during Trump’s self-imposed 90-day tariff pause. On Wednesday, after a meeting with Japanese officials, Trump claimed significant progress.

Japan’s chief negotiator, Ryosei Akazawa, confirmed that preparations for a second round of talks later this month are underway but added it was impossible to predict the outcome. It also remains unclear what kind of concessions Trump is seeking from Japan.

According to sources familiar with the discussions, the Trump administration is reportedly pressuring countries in trade talks to curb commerce with China.

While dozens of nations seek exemptions or relief from Trump’s historic tariffs, the U.S. is expected to demand steps that would limit China’s industrial capacity and prevent it from circumventing the tariffs.

U.S. Treasury Secretary Scott Bessent confirmed these reports, stating that he envisions agreements with Japan and other U.S. partners to launch a collective economic pressure campaign against China.

The move underscores Trump’s attempt to rally allied support in his economic offensive against Beijing. Whether this strategy will bear fruit remains uncertain, and doubts persist regarding the likelihood of successfully concluding any trade negotiations.

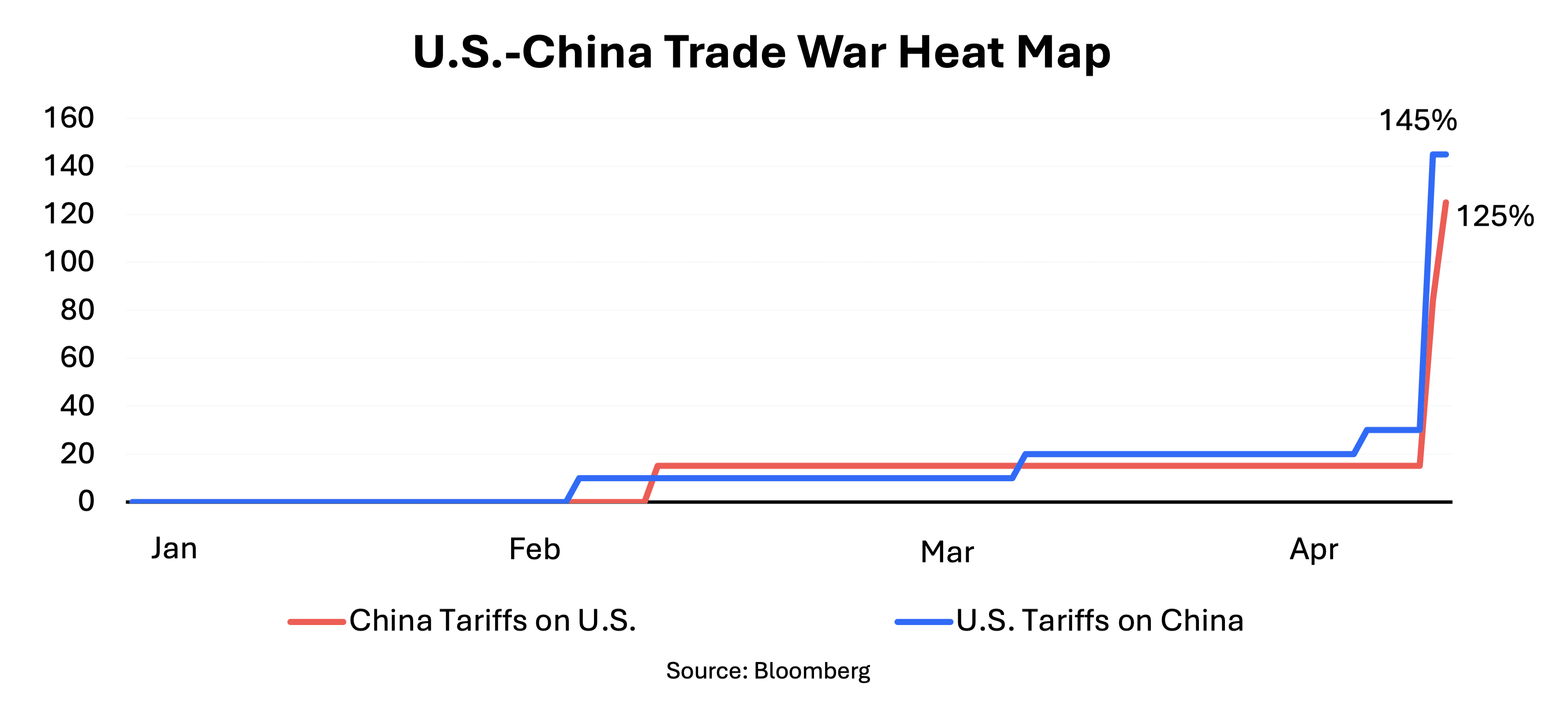

Meanwhile, uncertainty continues to cloud potential talks between the U.S. and China, which are currently locked in a tariff standoff exceeding 100% on both sides.

While Trump initially insisted that China initiate contact, Beijing demanded respectful engagement and expressed frustration over the lack of clarity in U.S. demands.

On Thursday, Trump claimed China had made multiple attempts to broker a deal, but he deflected questions on specifics. He also said he was hesitant to impose further tariffs on China, acknowledging that doing so could bring trade between the two countries to a halt.

In a contrasting move, the U.S. Trade Representative unveiled a new plan Thursday proposing fees on all Chinese-made and Chinese-owned ships docking at U.S. ports. According to a petition filed under Section 301, the fees—initially $50 per net ton or based on a vessel’s revenue-generating area—would go into effect within six months and rise gradually over three years.

The rationale is to reduce U.S. dependency on China’s dominant shipping role. However, if implemented, the measure would function as a de facto tariff, potentially disrupting trade and adding new cost pressures.

Meanwhile, Trump said he expects to reach a trade deal with the European Union but sees no urgency to finalize it.

However, sources speaking on condition of anonymity noted that if no agreement is reached, the EU is considering retaliatory measures, including export restrictions, expanded tariff lists, and limits on public procurement opportunities for U.S. firms.

In short, negotiations are taking place—but uncertainty lingers as to which countries will reach deals and where trade tensions may escalate further.

Tariffs Begin to Bite: Input Costs Climb, Outlook Dims

Although reciprocal tariffs on the EU and around 60 other U.S. trading partners have been paused for 90 days—with a baseline 10% still in place—sector-specific duties and the 145% tariff on Chinese goods are already affecting U.S. consumers and businesses.

According to government data released Wednesday, retail sales rose 1.4% in March from the previous month, driven largely by a surge in auto purchases—which are now subject to a 25% tariff.

In addition, many U.S. companies, even those that manufacture domestically, rely heavily on imported inputs and warn that higher costs will soon begin to filter through to prices.

While some are seeking alternative sourcing options, these transitions will take time and may not offer clear solutions.

As a result, both consumers and businesses broadly expect tariffs to accelerate inflationary pressures and weigh on economic growth. If both effects materialize, the U.S. may face a stagflation scenario—something the Federal Reserve will find extremely difficult to navigate.

Markets are increasingly pricing in more than three rate cuts from the Fed this year as growth risks mount. However, Fed officials continue to prioritize inflation risks and signal a preference to stay on hold until more clarity emerges.

Price Stability First: Fed Signals Caution on Rate Cuts

Federal Reserve Chair Jerome Powell reiterated on Wednesday that the central bank must ensure tariffs do not trigger a sustained rise in inflation.

He emphasized that policymakers will balance their dual mandate of maximum employment and price stability, stating that without stable prices, it would be impossible to achieve lasting labor market gains that benefit all Americans.

Economists interpreted these remarks as a sign that the Fed now views price stability as a prerequisite for delivering on its maximum employment mandate.

During the Q&A session, Powell added that both inflation and unemployment are expected to move away from the Fed’s targets for the remainder of the year. His comments aligned with the widespread belief among economists that tariffs are likely to raise inflation while slowing growth.

Powell also noted that the level of tariff increases announced so far is significantly higher than previously estimated. As such, during the Fed’s upcoming June meeting—when it will update its economic projections—it is likely to raise its inflation forecasts and lower its growth expectations.

As Duhani Capital Research team, we assess that based on Powell’s recent remarks and those of his colleagues, the Fed will prioritize inflation risks and wait for greater clarity on the economic impact of Trump’s policies. Accordingly, we expect the Fed to deliver just one rate cut this year—or at most two, provided inflation does not materialize as feared in the second half of the year.

Institutional Confidence at Risk as Trump Targets Powell

While Fed officials continue to emphasize their intention to keep interest rates steady in order to address potential inflationary pressures, they are facing renewed criticism from President Trump.

Expressing disappointment over the lack of rate cuts, Trump questioned the Fed's independence and remarked, “If I ask him to, he’ll be out of there,” in reference to Chairman Jerome Powell. He also argued that interest rates should be lowered, stating there is “essentially no inflation.”

Although a president cannot legally fire the Fed Chair, any attempt to do so could cause significant and lasting damage to already fragile confidence in the economy and financial markets—likely triggering a wave of market turbulence.

Gold Shines, Dollar Slips: Markets in Flight Mode

Tariffs, uncertainty, and Trump’s back-and-forth remarks are causing investors to question the safe-haven status of U.S. assets. This week:

The dollar declined by 0.65% against major peers

U.S. Treasury yields slipped

Equity markets extended their declines:

S&P 500 lost 1.5%

Nasdaq fell 2.3%

Meanwhile, demand for safe-haven assets remains robust:

Gold has gained nearly 27% year-to-date

Jumped nearly 5% last week alone

Hit a new record above $3,357 per ounce

Flows into the Japanese yen and Swiss franc have also stayed strong.

At the same time, data suggests long-term investors are beginning to view the dollar’s decline as a buying opportunity. According to custody giant BNY, net dollar inflows from institutional clients reached their highest level this year last week—suggesting some believe the dollar is nearing a bottom.

Conversely, data from State Street Global Markets shows asset managers are not yet underweight the dollar overall, indicating it is not yet oversold—potentially leaving room for further downside.

Ultimately, views on the dollar’s trajectory remain divided. But one thing is clear: global investors are in risk-off mode, seeking safety while closely monitoring developments in trade talks and tariffs.

With little progress on negotiations, this week’s low dollar volatility may quickly give way to larger swings depending on what comes next.